-

credit

The Difference Between Your Credit Score and Your Credit Report

If you’re an adult living in the modern world, you’ve most likely heard of a credit score. There are many companies out there that offer your credit score to you for free each month. (If you’re not already using one, check out Credit Karma and Credit Sesame, but be careful of all the credit card offers you’ll get from them!)

But do you know what your credit report is and why it matters? Your credit score and credit report are not one in the same, but they are both very important, and they will impact your financial present and future.

Your credit score and credit report are not one in the same, but they are both very important.

If you’ve read my past article about credit scores, you know the basics for why it’s important. But I’ll reiterate why you should care about your credit score:

Your Credit Report is a Picture of Your Financial History

Your credit report is basically a report card, but for your financial history. It will include the last 7-10 years worth of financial information associated with your name and social security number. This includes things like:

-

Name, address, birth date, and social security number (these are informational, not used against you)

-

Employment history (if it’s reported to credit bureaus)

-

Student loans and their status

-

Credit cards (both open and closed)

-

Any debts sent to collections

-

Hard credit inquiries (which is when you apply for a line of credit and the company pulls your credit report to see if you qualify for approval)

-

Tax liens

-

Car loans

-

Mortgages

-

Bankruptcy

-

Civil lawsuits

-

Any missed or late payments on any of the accounts listed above

As you can see, not all of these items are negative; they’re just facts. Your credit report is supposed to be a factual explanation of your financial history. It’s basically showing creditors and lenders whether or not you can be trusted with their money.

Your Credit Score is Influenced by Your Credit Report

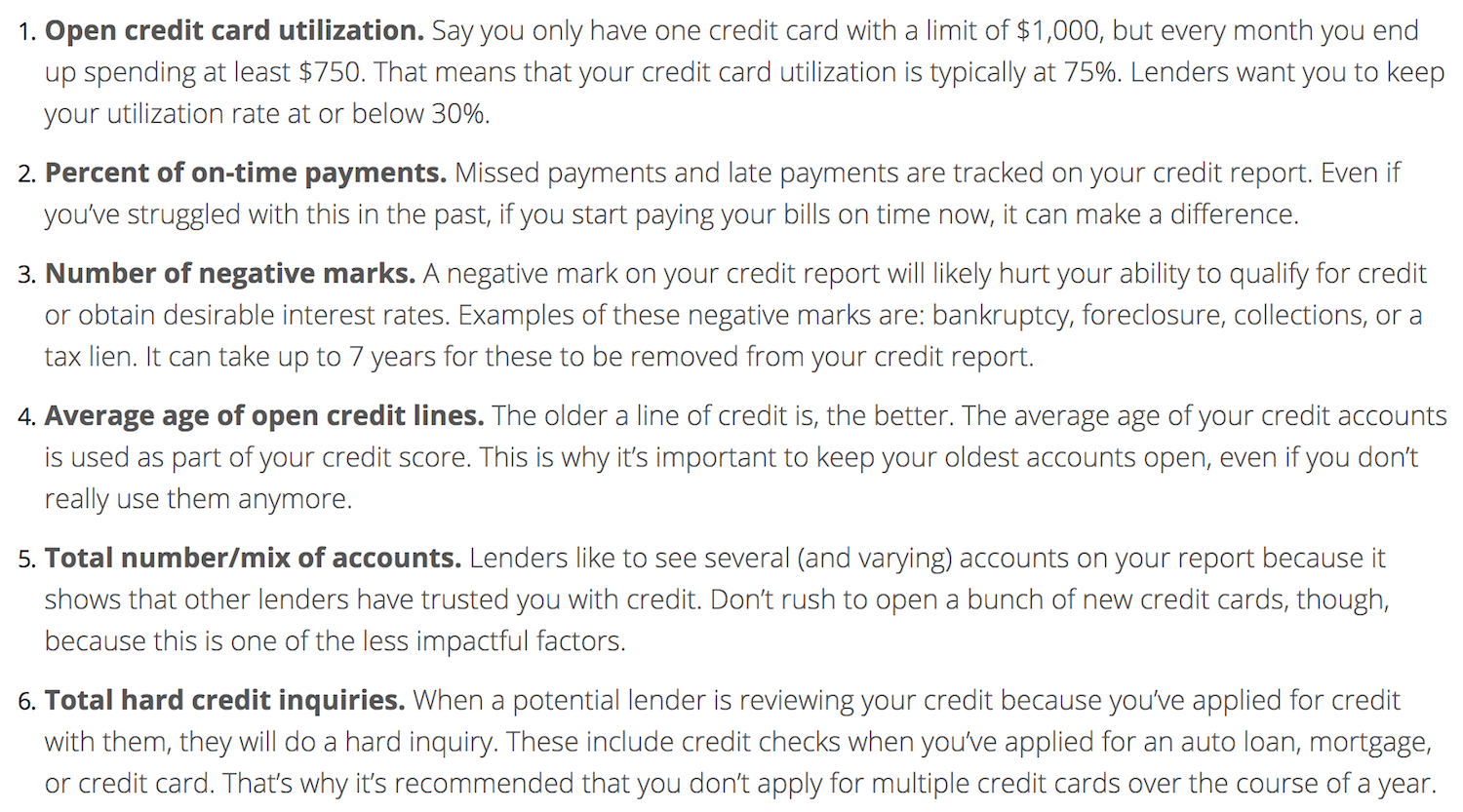

The information listed on your credit report will influence your credit score. For more in-depth information about what impacts your credit score, read my past post. But here’s a refresher on what impacts your credit score:

These different factors matter at different levels. Missed payments and negative marks matter the most. Credit utilization is next, meaning how much of the available credit you’re using. The length of your credit, number of recent inquiries, and the mix of your accounts matter the least when determining your score, but they do still matter, so keep that in mind.

Credit Bureaus are Legally Required to Provide Your Free Credit Report Annually

Do you remember that commercial where a guy would sing “free credit report dot com”? Well, he was lying because that service isn’t free. You have to give them your credit card information and then you get charged for a subscription. But there is an actual way to get your credit report for free.

All three credit bureaus are required to provide your free credit report to you once a year. The credit bureaus are Experian, Equifax, and Transunion. If you want to pull your credit report from them, go to www.annualcreditreport.com. I like to get a copy of mine every four months, since that means I’m getting one from each bureau each year, while spreading it out in case anything changes throughout the year.

Your Credit Score Can Fluctuate Often

Have you ever looked at your credit score and noticed that it’s 20 points off from where it was last month? Me too! This can happen for many reasons. For me, my score fluctuated the most when I was applying for a mortgage. There were multiple credit inquiries from lenders, and I had also applied for a credit card in recent months. There was so much activity happening on my credit report, that my credit score took a hit. Luckily, as things change and time goes on, your credit score can recover, as mine did.

Your Credit Report Takes Longer to Change

If you have any negative marks on your credit report, it can take up to 10 years for them to be removed. If you’ve missed a credit card payment, had a bill sent to collections, or filed for bankruptcy, it will show on your credit report for almost a decade.

Just because it takes time for your credit report to recover doesn’t mean that you shouldn’t try to improve your situation! See below for what you can do next to improve your credit score.

Of course, if there is a negative mark that you don’t believe belongs to you, you should take action! Sometimes, credit bureaus and creditors make mistakes. They may put something on your credit report in error. Or, more sinister, someone may have stolen your identity and racked up debt in your name. If either of these is true for you, you should contact the credit bureau and have them start an investigation. You should also reach out to the creditor directly and ask them to correct the issue with the credit bureau themselves.

So, What Should You Do Next?

You should check your credit score and credit report regularly! Your credit score will be updated every month at least. Sign into one of the free websites I mentioned above once a month and see how your credit score is doing.

Since you can only get your credit report for free three times a year, set calendar reminders for yourself. I have an annual recurring calendar reminder for each credit bureau, so that I know when it’s time to get my free report from each of them. For example, I pulled my Transunion credit report in May, so I have a calendar reminder set up for next May. I will pull my credit report from one of the other two bureaus in about four months to make sure everything is in order.

Once you have your credit report and credit score, you can start taking action. If you see any errors, file a complaint with the credit bureau. If you know you have a bill that could be sent to collections soon, pay it (or set up a payment plan)! Start making your monthly payments on time, and try to pay over the minimum in order to get your overall balance down.

Good luck!

More Resources:

-

https://www.nerdwallet.com/blog/finance/credit-scores-change/

-

https://www.creditkarma.com/advice/i/what-affects-your-credit-scores/

-

https://www.maggiegermano.com/blog/care-about-your-credit-score

-

https://www.maggiegermano.com/blog/check-your-credit-report